Attention flows to hot markets. Depending on when you look around, that could be AI, crypto, web3, climate tech, SaaS, Fintech, metaverse, VR/AR, or whatever’s trending now. But what if the best startup opportunities are actually in cold markets that most people ignore?

I wrote about a version of this phenomenon in my Why Now book, where investors rush into hot markets or, conversely, avoid markets that previously burned them even when the timing is finally right.

But there are some reasons to reconsider cold markets. The best companies often aren’t built in hyped markets. They’re built in ignored ones before they take off.

You’ll also see: + Less competition. You’re not fighting multiple VC-backed startups for the same customers. + Capital discipline. Less pressure to burn cash just to keep up. + Founder attitude. Tougher conditions force better problem solving and creativity.

The trick isn’t just to chase cold markets, but to find cold markets on the verge of heating up. Look for underlying shifts – technological, regulatory, behavioral, or something else (I track 12 timing drivers) that signal a coming change and how those changes can improve the legacy business model.

You also do need to be willing to look foolish or unfashionable for a while. But if you can stomach that, there can be opportunities for you in cold markets. The trick is to find the ones on the verge of heating up.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

If you’ve been following me here, you know that I spent the last couple years workshopping, speaking, and writing about the impact timing has on the success of a product. In extension of that, the following is an overview of different approaches I’ve found of others dealing with the timing question.

The following is an overview of some of the different timing approaches I found. These and other thinkers, as well as a lot of direct contact with businesses trying out these ideas, helped me make what I believe is a useful book.

And as a result, this is the only book completely focused on how timing impacts a business’s success and what you can do about it. Whether for startups pitching for funding, product people evaluating what to build next, investors making funding decisions, and corporate teams deciding where to put resources… The book provides a way to step through these decisions, successful and failed timing examples, and patterns of outcomes to gain insight.

Each is worth exploring on its own. But I’ll leave that to you. Rather than go into these in the detail they deserve, I’ll leave you with brief introductions here. Read Why Now: How Good Timing Makes Great Products for more detail on many of these. (But really read the book for how you can approach your own timing situation and benefit.)

1. First-mover Advantage / First-mover Disadvantage (Marvin Lieberman and David Montgomery). First-mover advantage was a term casually thrown around starting with the Dotcom era, though the authors never wrote that it existed as claimed. Convince your investors that you had first-mover advantage (in practice just being able to claim that no one else had tried to do the thing… on the Internet).

The joke about first-mover advantage is that the authors of the 1988 paper that popularized the term found that their work had been twisted into all sorts of directions, many of which had nothing to do with their research. On their paper’s 10th anniversary they wrote a follow-up article on first-mover disadvantage and also edited some of their earlier claims.

Those updates gained little attention in 1998. We were moving to the height of the Dotcom / Telecom bubble era back then. First-mover advantage all the way!

2. Adjacent Possible (Stuart Kauffman). Kauffman takes an anthropological approach to this topic. As we invented more tools, those tools could be combined in more ways. Once you reach a certain point, the plethora of combinations leads to an explosion of creation.

Kauffman also provides a formula that describes the phenomenon.

3. Inflection points (Pete Flint). Why do we see rapid growth in certain technologies or industries? Inflection points can explain part of that.

This is something that humans tend to be poor at estimating. We historically experience the world linearly. Day to day changes are modest until… wham! We’re surprised by the sudden explosion of something new.

4. Creative destruction (Joseph Schumpeter). The concept describes the way that innovation destroys the legacy ways of business, along with it the legacy industries, companies, and jobs, and creates new ones.

5. Wheel of Fortune (original meaning, not the game show). The wheel of fortune is the concept that we (individuals or groups) go through ups and downs over time. The pauper turns into the king. The wealthy tribute state turns into the impoverished backwater.

6. Dominant design (James Utterback). How do early industrial decisions constrict later options? The emergence of a dominant design explains some of that. Utterback describes a process where new innovations go through different phases. There is the fluid phase, where new options compete with each other; the transitional phase, where a dominant design wins and businesses now compete to meet demand; and finally the specific phase where innovation is low and the focus is on quality and cost cutting.

Examples include the layout of the Qwerty keyboard (not designed for speed typing), the calculator keypad with its different layout from the phone keypad, and the enclosed steel automobile body.

7. Startup Market Opportunity Curve (Rizwan Virk). Virk explains industry-specific investment as part of a cycle. At the beginning there is lots of risk and little investment which is hard to raise, then lots of risk and lots of investment during which it becomes easier to raise.

The insight is in applying different tactics depending on the stage of your industry rather than consistent tactics throughout.

8. Flywheels (Jim Collins). How you can conceptualize an overall accumulation of effort that produces improving results. Get the flywheel spinning and it helps you spin it faster.

9. Portfolio company study (Bill Gross). This comes from a short TED talk and a couple other references. The founder of Idealab (an early incubator) analyzed 200 companies on the idea, the team, the business model, funding, and timing. Gross then estimated that 42% of company success was due to good or bad timing. He didn’t share his data or process, but it’s an interesting reference point. But contrasting his model and mine, I interpret four out of five of his categories as being related to timing.

To compare, I looked into companies I’ve worked with to see if timing held up as a success or failure factor. It did.

I looked at the largest portfolio of startups I’ve been involved with, from the incubator at the University of Southern California. Of the 168 companies from that portfolio that have been stable enough to survive for at least two and a half years (range two and a half to nine years), the failure rate was 51% for those with a timing advantage but 70% for those without a timing advantage. It was even more extreme in the acquisitions. Eight out of the nine acquired had timing advantages.

10. Installation periods / Deployment periods (Carlota Perez). Perez describes macro forces of government and category investment that lead to innovation, cost declines, and more.

11. The Multigenium (John Lienhard). Inventions come from individuals, but the “multigenium,” the many creations that enable other things to be invented, itself comes from the collective action of many.

12. The Inevitable (Kevin Kelly). Wired co-founder Kevin Kelly introduces a set of 12 inevitable changes we will see in the coming decades.

13. Moore’s Law in Reverse (Alan Kay). Alan Kay, of Xerox PARC describes the process they used to invest in futuristic computers for team members: “run Moore’s Law in reverse.” That is, rather than wait for the performance per cost curve to run its course, pay extra and get that computing power today. On those “machines of the future” you can build futuristic things. If you work with machines of today, you’re really working on technology of the past, which already passed through the Moore’s Law performance improvements.

14. Hype cycle. A visualization of the ups and downs of attention and expectations for new tech, as popularized by Gartner, with the following stages: On the rise, At the peak, Sliding into the trough, Climbing the slope, Entering the plateau.

A few years after the dotcom and telecom bubbles burst I attended a talk by the CTO of a large infrastructure company that saw its stock price skyrocket and then fall back to earth. He spent a lot of time talking about the hype cycle, referencing the railway industry of the 1800s. A nice history to know.

No one asked him why his own company rode it all the way up during the bubble and then all the way down. Not even me.

15. “Cambrian” explosions. There have been multiple eras of explosive creation throughout natural history. The Cambrian explosion was one of those, during which a large number of new species emerged. Why do these diversification periods happen in nature and why in the human-built world?

16. Tech/infrastructure leapfrogging. This largely depends on regulatory, economic, and geographic arbitrage. A common example: in some parts of the world, there never was a strong legacy fixed line telecom network. It was expensive and hard to get a landline.

So when wireless technology became good and cheap, deploying mobile networks and phones leapfrogged over the existing poor fixed line networks. In other countries that had strong fixed line networks, mobile phone penetration took longer. People already had easy telecom access.

17. Crossing The Chasm. Book by Geoffrey Moore that describes the way new products can reach the mainstream market. More about finding the path than timing, but it helps explain why a new product takes time to popularize, depending on the actions of its promoters.

There are more examples I could add, but this gives you an idea. People have been interested in the “why now” question for a long time. I hope that my Why Now book proves helpful as you think through timing and how you will act on it.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

They say timing is everything in business. In fact, in a survey of 800 VCs, timing was one of the top reasons they noted behind successful or failed investments. (And though it might seem counterintuitive, being early is often more dangerous than being late.)

But how do you determine if your timing (or “why now”) is right? I set out to learn more through research and testing my findings. Along the way I developed a set of helpful frameworks and a process that I bring investors, founders, and innovation teams through as they consider where to put resources.

Here’s a partial list of some insights and recommendations I developed along the way:

Look for what I call Timing Drivers. I track 12 types of drivers in a general sense and have teams I work with go into detail for their specific situations. The drivers I track include everything from the Technological (for example, performance curves and cost improvements), Installed Base (critical mass reached in users of supporting equipment and systems), Capital Access (sources and availability), and more. These drivers are a mental shorthand for where to look for environmental changes. These drivers are also most likely changes that are happening outside of your control. Some may have a level of predictability to them, while others may not. You notice change and then put your perspective behind what’s changing.

Connect the Timing Drivers to your potential business model. Timing Drivers need to improve an existing business model or make a new one possible. Otherwise, you don’t have a timing advantage. You only have a new capability that is at risk of being financially unsustainable. Companies that skip this step can end up wasting the money they raise because what they’ve built may never produce enough value for customers or may never enable the business to capture enough value back from their customers.

Timing shifts your market size. If we’re not simply evaluating an unchanging, well-understood market, then we should think differently about the role that timing has in potential market size. Too often we look at markets as being measurable and static or as undergoing dramatic growth, but don’t understand what produces that static or dynamic market. Timing plays a part here. In the year 1900 you can’t estimate the market for cars by extrapolating from the existing number of horses.

There are “Timing Patterns” we can learn from. These are repeated combinations of timing drivers that offer us examples to learn from. I’ve written about some of the most common I’ve observed. These patterns help give us a starting place to look for potential timing advantages.

Run “Why Now Sessions” and build “Timing Maps.” These are processes and tools I developed to conduct a structured evaluation of a market and industry to identify whether this is a promising time for a specific concept. The Timing Maps visually represent the factors influencing your timing decision.

Don’t simplify too much. For example, while people often say you should “sell shovels in a gold rush,” think about what type of situation you’re actually in. There are different types of allegorical shovels you can sell, just as there are times when it is more beneficial to mine for the gold. The original discoverer of gold at Sutter’s Mill, James W. Marshall, died penniless. So did Samuel Brannan, the proprietor of the only general store near Sutter’s Mill (he sold lots of shovels). But one seller of “shovels,” Levi Strauss, the first manufacturer of tough denim jeans, did much, much better. Consider which shovel seller (or gold miner) type you might be.

Consider how early you should enter. This depends on how long you expect it will be for the market to be ready, just as it also depends on the type of organization you are. Are you able to build quickly and benefit even if the market window may quickly shut? Or are you better off watching first entrants, learning from their mistakes, and then entering? This requires you to evaluate your own business as much as it requires an analysis of the external environment.

Remember that first movers usually fail. If you plan to be a first mover, can you control resources to make it more difficult for later entrants? Can you lock in customers? If not, what will prevent later entrants with better products from overtaking your business? Too often, in our excitement to enter a new market, we don’t consider these long-term questions.

As you can see, there are many timing-related considerations. I spent the past few years focused on the timing question and issues like those above and distilled my findings into a concise, practical book. The book is called Why Now: How Good Timing Makes Great Products.

This book is your guide to understanding the drivers of good timing, the impact timing has on business models, and how to apply these insights to your unique situation. Whether you’re an investor, founding team, product manager, or part of an innovation group, this book offers valuable frameworks and real-world examples to evaluate and leverage timing in your ventures. I hope you enjoy it.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

10 years ago today, NYU finance professor Aswath Damodaran, well-known for his work on corporate valuations, posted an article on Uber. The rideshare company was already a unicorn (a new term at the time), with a $17B valuation.

Yet, Damodaran ran the numbers and came up with a more modest $5.9B valuation. The title of his post, “Uber Isn’t Worth $17 Billion” summed up his thoughts. Lest we forget, many others back then also thought that companies like Uber (as well as other unicorn startups) were overvalued.

A month later, Uber investor and board member Bill Gurley posted a rebuttal. In “How to Miss By a Mile,” Gurley laid out an argument for Uber’s valuation.

But you have to appreciate Damodaran’s analysis. He showed his work and provided his Excel model. Gurley, on the other hand, revealed fewer numbers or didn’t want to share specifics for a then-private company.

To be fair, Damodaran had to rely on public information where Gurley had insider knowledge. But the main difference between the two approaches was on whether the world would remain the same in the future related to local transportation (the Damodaran model) or whether the world of transportation would change in a meaningful way (the Gurley model).

But how could you ever know if the world is ready for change or if things would largely remain the same?

Questions like that involve the role of timing.

Timing Changes The Market Size

As part of his process, Damodaran estimated the market size of the global taxi industry. He summed up measures of the largest taxi markets in the world (Japan, UK, USA) as $50B and doubled that for the rest of the world. This estimate came to $100B/year, with the large markets like the US stable and real growth coming from emerging economies. He averaged annual growth at 6% / year, meaning that the taxi market that he put Uber into was projected to grow to be $183B by 2024.

Among the logical mistakes I believe Damodaran made was in believing that (as he wrote): “Unlike technology companies in other businesses, like Google, Facebook and eBay, the network effect and winner-take-all benefits are limited. Having a global network of tens of thousands of cabs doesn’t make a difference to a customer looking for a cab in New York City. That, along with the regulatory restrictions protecting the status quo and the competition Uber faces from Lyft, Hailo and others, lead me to estimate a market share of 10 percent.”

Let’s look at why these assumptions proved to be incorrect.

Uber didn’t immediately roll out drivers around the world. They intentionally rolled out new geographies when they could manage (and create) supply and demand. There are winner-take-all benefits even for rideshare, whether from the view of passengers (don’t need to find the local rideshare app for each trip) or from the view of the rideshare companies (accrued benefits to the tech, mapping, funding of new market expansion).

Damodaran also overestimated how much power municipalities had to prevent Uber from entering their cities. Uber’s tactic here was to enter without permission, provide service better than the baseline taxi companies, gain passenger support, and then negotiate with municipalities that wanted to force them out.

In his model, Damodaran took the 10 projected years of free cash flows, the estimated terminal value after year 10, assumed that Uber would cap out at 10% of the overall market size, and that it would take 10 years (that would be 2024) for the company to reach that stable state.

Way too small to read as an image. Check out the actual spreadsheet.

When it came to VC Gurley’s rebuttal, he used this short description of why projections can mislead.

Sizing the market for a disruptor based on an incumbent's market is like sizing the car industry off how many horses there were in 1910.

Seeing that Tweet, I looked at the markets for horses and cars when doing research for my Why Now book. It tells the story. The market for cars does not cap out at the size of the previous market for horses. Rather, the market for cars becomes much bigger than the market for horses. The market for cars opened up new transportation possibilities.

Gurley focused on some key differences between the legacy taxis and new entrant Uber. With Uber, pick-up times were faster, there was improved “coverage density,” or the ability to grow the service area, there was no need for cash payment, having driver and passenger ratings produced better behavior, and resulted in higher trust and safety.

Gurley claimed that Uber was highly price elastic, meaning that as it lowered its prices, more people would choose it, even choosing it over other options, such as not traveling at all. When Uber would start to strategically alter its pricing, it would benefit from that price elasticity.

Gurley provided other use cases in Uber’s favor, but stressed the potential for the company to be an alternative to owning a car. In the US, few cities have such good public transportation as to eliminate the need for a car if you could afford one. But Uber’s entrance potentially does just that.

Interestingly, Damodaran’s 2014 estimates of what the taxi market size would be in the year 2024 ($183B) wasn’t that far off from more recent estimates ($230B in 2023).

However, the sum of the taxi and ride-hailing markets became about twice what Damodaran estimated for 2024.

Uber’s market share of the combined ridesharing and taxi market ended up being 25% globally, as opposed to Damodaran’s assumed 10%.

Since those previous projections are now history, I used Damodaran’s model and plugged in the actual numbers for 2014 – 2024 for the taxi and ride-hailing markets and increased Uber’s market share to 25%. Writing in 2014, Damodaran obviously didn’t factor in a market decline for Covid. So I went back and smoothed the growth rate for the years 2020 to 2024.

Damodaran’s valuation after those changes? $28.4B, or almost five times his original estimate. Uber’s last valuation before IPO was $80B. Current market cap is $135B.

But what changed the market size? I think about this in terms of timing.

The general process I follow is to look for Timing Drivers (there are 12 I consider), to understand how those Timing Drivers impact the company’s business model, and then to consider what company is best positioned to take advantage of those changes.

Rideshare businesses only because possible around the year 2009 or 2010 when Uber launched. Timing Drivers that enabled their existence included critical mass of smartphones with GPS chips that were fast enough to provide turn-by-turn directions, user comfort with online payments and ratings systems, and gig economy demand. While pieces of those Timing Drivers existed earlier, their combination was essential.

Those Timing Drivers combined to enable a new business model. Namely, a business model where Uber could provide higher value to customers (clarity on when a car will arrive, driver trust, no need to carry cash), revenue for the business (charging passengers’ credit cards), and lower per ride costs (car and fuel costs are pushed to the drivers, while Uber provides the overall system).

Avoid Damodaran’s mismeasurement. Go through what I call a Why Now Session to evaluate the future potential for a new business or evaluating whether it’s the right time for a specific product or service to grow. I describe the process, with frameworks and examples in the book Why Now: How Good Timing Makes Great Products.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

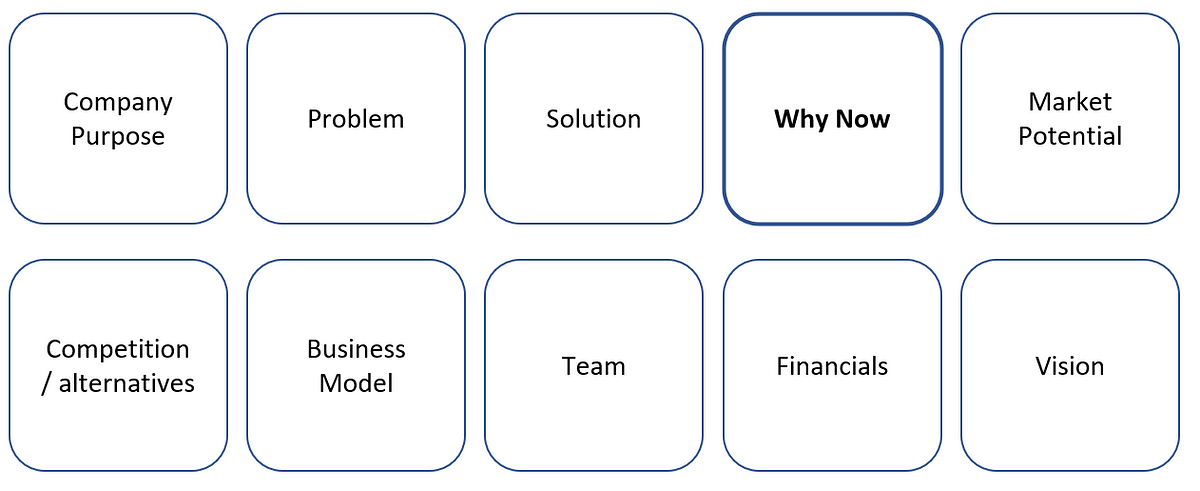

Now let’s look at the way people have presented timing advantages. Below is a collection of:

Why Now slides from pitch decks (26 examples)

Sequoia startup founders on the Why Now question (6 examples)

Interviews with founders, investors and more about timing (12 examples)

Weak Why Nows and companies that failed because of or in spite of timing (6 examples)

Why Now slides from pitch decks

I believe that your perspective on timing is one of the most important pieces of insight you can bring to the discussion with an investor or when discussing resources and direction internally.

As I demonstrated in the earlier posts above, you need to do your own research to have a perspective. And while you’ll summarize your timing advantage in a single slide, you should start with that more detailed research. Otherwise, you won’t be able to answer investor and management questions (and your slide will be superficial).

Powerful startup Why Now slides explain why this business is in the market at the right time (and why a few years ago would have been too early). What has changed? What timing drivers opened up a market window that the startup is now exploiting? The slide is typically placed after the problem and solution slides.

This is a collection of slides from actual startups, all publicly available online. I show just the relevant slide the company used in their deck and also add a quick assessment.

I take the slides at face value but I’m not claiming that these examples are perfect. In some cases I critique them or question the assessments. This is an exercise to understand how startups expressed their own timing advantage. In some cases, I show how the Why Now assessment ended up being incorrect.

The images link to the full decks.

AdPushup

Comments: This slide relies on analyst forecasts and (at the time) hotness of the adtech market. If you can move fast, you might be able to take advantage of a hot market. But if things outside of your control change, what do you do then? Think a step earlier to what drives the expected growth. The A/B Testing comment is more focused on open space in a market where experience from another market can be applied.

Bliss AI

Comments: Interesting from today’s perspective that Bliss AI was focused on remote work back in 2015 and listed a projection for the year 2020. Rather than use projections of how big remote work would become, think about what drives the change.

Crossbeam

Comments: This is a list of strong drivers that demonstrate why the time is right. The slide also shows how the drivers collide to produce an even stronger effect. Go into more detail on expected growth in due diligence.

Databricks

Comments: Connecting the need to build AI/ML solutions with these four categories makes this a strong slide. The commoditization category is especially interesting.

Dropbox

Comments: Good list. In discussion, the founders can explain just how cheap storage and bandwidth have become (this slide is from 2008) and how that makes a new business model possible.

Dutch

Comments: Good assessment of what changed because of the pandemic, how that impacts pets, and what will further change when people go back to the office rather than work at home.

Enduring Planet

Comments: This startup makes make rapid financing available to climate entrepreneurs. Is the focus on the interest in climate change enough of a timing driver? They also provide a simple diligence and investment process which isn’t common. Could they claim that tech also adds to their “why now”? This is one of the simplest Why Now slides I’ve seen. It could go a lot further.

Fivetran

Comments: Good list, but what is changing with these tech drivers? Why wouldn’t this business have worked a few years ago?

Glambook

Comments: Rather than quote a projection, what drives the increase in self-employment for their targets? It’s unclear what will change by 2027. Weak slide.

Harvest Money

Comments: Do these numbers represent a tipping point? Were the debt numbers of a few years earlier too low for this business to be built? Otherwise, if it didn’t matter in the last recession, why is it different now?

Kahani

Comments: Might be a good opportunity, but I’m not sure about the why now claims. Why did mobile ecommerce survive so long without changing? Seems more about straightforward performance of this solution. Why are ecommerce sites going to change now?

Lunchbox

Comments: The driver is entirely about existing and projected market size. What else is relevant here? Why will this market growth continue? Will growth continue post-pandemic?

Lunch Club

Comments: It’s a list, but if these changes have been ongoing, why do they matter now?

MetaCert – In-App Security

Comments: Interesting point that thanks to the growth in DIY app builders there will be demand for security, or at least fixing security problems. (But if the point is that creation is exploding, I don’t see it in the image.)

MetaCert – Team Collaboration Security

Comments: This would be stronger if it explained how this risk is growing. Haven’t companies dealt with this security risk for years at this point? What changed? Was a tipping point reached? A regulatory change?

Momentum

Comments: This slide is from 2022 and so it leaves a lot unsaid. Remote work and reliance on remote tools are now norms. Did this business require the Covid push to remote work?

National Virtual Observatory

Comments: Strong. These changes enable this business (slide is from 1999). Without these timing drivers the outcomes would be dramatically more expensive and less powerful.

On Deck

Comments: Strong list that supported their fundraising efforts in 2021. But did traditional higher education really decline as ed-tech grew? And while that Peloton example stings from the viewpoint of 2022, it did the job then they wrote this list. A strong Why Now also doesn’t mean that the team won’t mismanage their opportunity later on.

Party Round (now called Capital)

Comments: A simple slide that tells the story. Verbally fill in the details about how fast these alternatives are growing.

Shift

Comments: If the used car market has doubled in the last decade, will growth now slow down? Is the online research done more often today than previously?

Snyk

Comments: Good combination of timing drivers. The “New Kingmakers” one is interesting because it combines existing tech talent with a new responsibility.

Standard Treasury

Comments: Simple list. The big question is whether the company can move in line with the regulatory changes. What else about the tech maturity and growing market would be relevant?

Sunshine

Comments: The biggest timing driver here is the increase in smartphones with built-in sensors.

Supliful

Comments: These may be facts, but what changed? Was there a tipping point reached in number of creators? Did creators become more relatable than brands just recently? Otherwise, it seems that this business could have been started years earlier.

Vori

Comments: Many startups benefitted (or suffered) because of the sudden onset of Covid, lockdowns, and supply chain problems. If a business happened to be well-positioned to benefit from such changes or was able to adjust quickly, this crisis provided a strong timing advantage. The question is then what happens when things go back to the way they were?

Yapily

Comments: This is a full look at drivers behind this company’s existence. The main one is probably the regulatory change.

The following are interviews focused on the startup “why now” question that Sequoia investors did with their portfolio companies. Snippets of the conversation are below along with video links. These are all from 2018. The update comments are limited to additional funding rounds or acquisitions as a sign of whether the companies continued on the right track.

Wonolo (on-demand staffing for businesses)

“The problem of unpredictable staffing has been around forever. It’s not new. What’s new is that with the increasing adoption of mobile technology and the rise of the on-demand economy, we’re seeing a paradigm shift in that people are trusting an app to find workers and jobs.”

Update: Raised $140M in 2021, a few years after the above.

Front (customer communication platform)

“Before, companies were just using email to get organic and now they have Twitter and Facebook and Snapchat and text messages and so on. So they need to centralize everything in one place because those are just different ways to do the same thing: communicate. And that’s what Front does.”

Update: Raises a Series D at 1 $1.7B Valuation in 2022.

rideOS (mobility-as-a-service technology).

“As you look back at transportation over the last few decades, there’s been three megatrends that are completely changing the way that people and goods move throughout the planet. The first one was electrification. We had great companies like Tesla bring that technology to market. The second one was ridesharing and concept of sharing cars. And companies like Uber, Lyft, and Didi brought that technology to market. And a third one has been autonomous technologies. How to effectively utilize technology to drive on the road. And there’s been significant investments into the third bucket over the last few years. But most of that investment has been focused on how to get one vehicle to market. As we look towards the path that this technology is taking and we look at a world that is filled with millions of self-driving vehicles and other forms of transit, like buses, and MRT stations, and taxis, and also other forms of transport, there needs to be a type of air traffic control system for ground transport. And that’s where rideOS comes in. We’re looking at the problem of taking fleets to market and building marketplaces and mapping services to help bring that system to the world in a safe and efficient manner.”

“We’re at a unique time in technology where we have all these amazing component technologies that are very cost-effective today. To basically be able to allow an autonomous mobile agent to move very reliably and very safely through human spaces. That’s something that just wasn’t possible 10 years ago that is now very much achievable.”

“90% of our industry is comprised of small trucking companies, either owner operated or small fleet. Lack of transparency and yield mandates actually make our existing trucker shortage problem more severe now. And NEXT Trucking actually increases our carry efficiency by connecting them with their preferred loads and then we also help our industry supply and demand.”

Update: Later raised at a $500M valuation in 2019.

Snowflake (cloud computing)

“Because it really wasn’t possible to build Snowflake before now. The cloud made Snowflake possible and with Snowflake companies can work with vast amounts of data. And all of the people within an organization and even across organizations can work together.”

Update: Later raised another $480M and then IPO’d in 2020.

Interviews and Articles

This is a collection of interviews and articles where the timing question comes up.

Torc Robotics

“Why now for the automotive push? Torc CEO Michael Fleming told me that the time is finally right, both in terms of the state of available technology, but also in terms of the appetite for autonomous products from consumer automakers — which weren’t always as eager to develop and invest in self-driving.

“What we’ve found is that were some other markets that were early adopters to this technology, and there wasn’t a great deal of interest in the automotive industry coming out of the DARPA Challenge,” explained Fleming. “Google is really the early adopter of this technology, with some key folks from the Carnegie Mellon and Stanford teams from 10 years ago, and they’ve done some great marketing, and they’ve been on the forefront of this technology in the automotive space.”

Comments: The timing question here refers to Torc’s push into automotive, having already built other autonomous applications.

“Regulations can define the best places to build and invest”

“In April, the White House announced a target for the U.S. to reduce greenhouse gas pollution by at least 50% by 2030 and achieve net-zero emissions by 2050. The guidance includes a vision for more investment in building a transmission grid, electric vehicles and charging infrastructure, and carbon capture tools, and enabling farmers to foster sustainability in soil.

“In aggregate, the support of the public sector streamlines private-market solutions through access to alternative (often equity-free) capital and press recognition, which is crucial for a market that typically requires longer time to monetization and profitability.

“Ultimately, the regulatory fabric is an important market maker or breaker. That is true for nascent companies searching for answers to the “why now?” of market timing and also for established, public companies that are answering strategic questions of how much more they can grow.”

Comments: Regulations and top-down support are an influence on timing advantages.

“4 strategies for deep tech founders who are fundraising”

Answer the question of “why now?”

“Being right but too early or too late is the same as being wrong in the investing world. Early-stage venture capital investors operate on seven to 10 year time horizons with their investments because that is the timeline they have for each fund to return capital to themselves and their limited partners (those who invest in venture capital funds). If your company can only be a huge success 15 or 20 or 50 years from now, venture capitalists would still not invest because this return would not be realized on their target timeline.

“As a result, it is crucial to discuss not only why your idea is great but also answer the “why now.” Deep tech companies have more of a why now than companies in most other sectors. There are technological inflection points and regulatory tailwinds that make the timing perfect for deep tech companies.

“Dedicate a slide to explaining how macro and industry level tailwinds make now the ideal time to start your company. Articulate why your innovation could not have been achieved before today and why tomorrow would be too late.”

Comments: Framing timing in the seven to 10 year investment horizon is interesting. It’s also a reason that startups needing more time need to seek different investors.

“General Catalyst’s Niko Bonatsos on why timing and empathy are key to founder success”

“Q: If you were to pick one and only one single biggest factor that determines a startup’s success, what would it be? Why? Some say it is product-market fit (Marc Andreesen), others hold that it’s timing (Bill Gross) and yet more believe it is the team. Asked another way, what do you think is essentially different about successful startups?

“If I had to pick one, I’d pick timing. But again, it could be explained as foresight or genius of the founder to launch the startup at a great moment in time.

“The most successful companies have a confluence of factors aligning to work in their favor. Take Facebook, for example. Mark Zuckerberg founded it at a time when everyone was getting online and broadband was becoming pervasive.

“In contrast, some really talented and hardworking founders just happen to work on the wrong things and don’t attain the same level of success. Some even tried Zuck’s idea but were too early. It often isn’t their fault. The timing just wasn’t right.”

“Mural raises $23M Series A after history of capital-efficient growth”

“Gaddy also answered the why now, and why so much question, saying that Mural is riding a ‘secular trend in terms of how people are going to produce creative work.’

“Mural is a tool that can be seen as a remote-work-friendly service. It’s also workplace collaboration software, putting it smack-dab in the middle of two current trends in Startuplandia.”

Comments: This is from a January 2020 article, just before Covid sent work to default remote. Mural benefitted both from the long-term trend and the sudden crisis change.

“VCs have to train themselves to ‘ask the stupid questions,’ says Hoxton Ventures’ Hussein Kanji”

“I think it’s actually perfectly fine in the venture industry to not be the smart person and to kind of train yourself to be stupid and ask the stupid questions,” said Kanji. “I think a lot of people are probably too shy to do that. And a lot of people [are] probably too risk averse to then write the check when they don’t really understand exactly what it is that they’re investing into. But a lot of this stuff is a light bulb moment.”

“One of those light bulb moments was Hoxton Ventures’ investment in Deliveroo, the takeout food delivery service that competes with Uber Eats and helped turn almost every restaurant into a food delivery service. However, Kanji reminded us that the European unicorn wasn’t the first company to try takeout delivery, but new technology, in the form of cheap smartphones coupled with GPS and routing algorithms, meant the timing was now right.

“‘People did try delivery,’ he said, ‘they tried it back in the 90s. Everyone forgets about that. There’s a company in New York City called Kozmo that would go off and like get you a pint of ice cream on demand. You know, it never worked because they used pagers. Like, do you remember pagers?… The breakthrough for delivery, and for that whole industry, was you had smartphones, you could give smartphones to the drivers, you could track what the driver was doing, which is good because then you could route logistics, you know, with a smartphone… light bulb moment.’”

Comments: A common timing example involving GPS-enabled smartphones.

“YC-Backed SpinPunch Aims To Build Faster, Prettier HTML5 Games”

“Mars Frontier is certainly an impressive game (albeit one that I sort of suck at), but I had to ask: why HTML5? Why now? Tien thinks the shift toward building more compelling browser-based gaming experiences is a matter of course, but doesn’t see too many players in the space really trying to push HTML5’s limits….

“It’s just a matter of time before the entire games industry moves to the browser, since the distibution [sic] advantage is so powerful,” Tien noted. Though the potential for tremendous reach is there, the shift isn’t going to happen overnight, but SpinPunch seems intent on riding the bleeding edge until it does.”

Comments: A new technology driver coupled with existing demand.

“Fin names former Twilio exec Evan Cummack as CEO, raises $20M”

“‘Service teams were forced to go remote overnight, and companies had little to no visibility into what people were doing working from home,” she added. “In this remote environment, we thought that Fin’s product was incredibly well-suited to address the challenges of managing a growing remote support team, and that over time, their unique data set of how people use various apps and tools to complete tasks can help business leaders improve the future of work for their team members. We believe that contact center agents going remote was inevitable even before COVID, but COVID was a huge accelerant and created a compelling ‘why now’ moment for Fin’s solution.’”

Comments: Crisis as an accelerant on what was going to happen anyway. Crisis sometimes operates differently and makes a change in outcomes, rather than just speeding them up.

“Q3 2020 is primed to be an intense shopping season for VCs”

“You have to include a “why now” slide and it should mention COVID-19.

“We already know that investors respond well to a Why Now slide. Our research shows that 54% of successful pitch decks included a Why Now slide, where only 38% of failed decks included it. That slide now has to work twice as hard. We’re hearing from investors that they expect to see information in your pitch deck about how your business has been affected by COVID-19 and how you plan to manage that impact moving forward. Even if the pandemic has had no material effect on your business, the investor will still have the question. Get out in front of it with a well-formed response near the beginning of your deck.”

Comments: Seems obvious now, but Covid became the big change of 2020. Everything was filtered through that crisis.

“Nest Team Descends On Nike Town To Recruit Fuel Band Engineers”

“Nest, the connected device company that was acquired by Google for $3.2 billion, apparently needs all the hardware engineers it can get. As the core hardware group within Google, Nest will be spearheading the development of new hardware products.

“That could mean phones, or tablets, or… wearables?

“So it’s probably not a surprise that members of the Nest team paid a visit to Beaverton, Ore. yesterday to have an informal meet-and-greet with folks who might have been part of the Nike Fuel Band team….

“Which is why now is a great time for other hardware companies to give them some options, by trying to recruit them.”

Comments: Good to move quickly when a crisis (the Nike lay-offs) combine with a lack of talent in a specific desired domain.

“Whistle While You Scroll, Or, How Facebook Could Conquer Music Videos”

“Suddenly, it seems like everyone wants to host music videos. Apple features them in Apple Music, both as suggestions of what to listen to and as posts from artists in the Connect tab. Spotify recently announced it would start showing video clips inside its app. New apps like Vessel are trying to court indie musicians and their videos with better revenue sharing. The labels still run their own hosting platform Vevo that often fueled by YouTube’s player. And YouTube is trying to monetize music videos more aggressively with its YouTube Music Key ad-free paid subscriptions.

“Why now? Mobile has come of age for video. Phones unlock the little five-minute wait times in our lives, and prime them for content consumption. Faster network connections, bigger screens, and more powerful processors all mean the videos load and look better. And advancements in mobile advertising make them monetizable.”

Comments: This article was written in 2015. Since then, Facebook did go much more heavily into video, but also faced competition from other video-first companies.

“The “Why Now?” helps us understand the market conditions that now make it possible for the potential investment to have global impact. We’re looking for cash-efficient disruption of large existing markets or the creation of new ones. Broadly speaking, we invest in technology companies that are taking advantage of mobility and data. Mobility to us means not just the rise of the smartphone as the dominant computing platform, but also new technologies such as Virtual Reality and Augmented Reality (VR/AR). Data doesn’t just mean Hadoop, it also means companies that are helping others take advantage of the huge surge in all different types of data being collected or delivered (from commerce to commuting to mobile video delivery). Many of the sectors we invest in are just starting to tap into their potential for huge impact, including transportation, fintech, commerce, VR/AR, big data, mobile SaaS, and AI. Check out the ideas section of our website for other areas we’re looking at.”

Comments: From 2016, this article focuses on the way an investor looks at timing.

Having a timing advantage is not a guarantee of success. There are lots of ways to miss an opportunity. We also have to be sure that we don’t just cherry-pick the best examples.

But there are also lots of ways to invent a timing advantage when there are none. Is there anything in common when we see this happen?

“Source: Facebook Is Testing ‘Facebook At Work’, Separately Hosted Version To Roll Out In A Few Months”

“Enterprise social tools have existed for years. When I asked why now, the source told me it was simply because Facebook now had the infrastructure in place to support such a system”

Comments: The infrastructure rationale is weak. If Facebook didn’t have the infrastructure, would they built it for this product?

“Timing, more than anything else, is what I think is to blame for our unfortunate fate. Our approach, I still believe, was the right one but the space was too overwhelmed with the unmet promise of AI to focus on a practical solution. As those breakthroughs failed to appear, the downpour of investor interest became a drizzle.”

Comments: In my other work on the timing topic, this is where we see the expectation of a process that seems to be improving on an exponential curve instead flattens into S-Curve. The needed improvements are still years away. Early companies shut down or burn cash seeking the improvements they need to bring their product to market.

Vreal

“VR platform Vreal intended to build a virtual reality space for video game streamers to hang out with their viewers and raised almost $12M in its 2018 Series A. However, the available hardware and bandwidth capabilities didn’t evolve as fast as the company had expected, and though it delivered on its promise, Vreal struggled to attract any significant usage:

“Unfortunately, the VR market never developed as quickly as we all had hoped, and we were definitely ahead of our time. As a result, Vreal is shutting down operations and our wonderful team members are moving on to other opportunities.”

Comments: I read this as mostly the result of a lack of demand. What could have given the team and investors this insight ahead of time?

Stockwell AI

“For some companies on our list, an unforeseen factor like the Covid-19 pandemic contributed to product untimeliness. AI-powered vending machine startup Stockwell AI shut down in July 2020 as consumers stayed at home and avoided surface contact. The company’s CEO Paul McDonald wrote in an email to TechCrunch,

“’Regretfully, the current landscape has created a situation in which we can no longer continue our operations and will be winding down the company on July 1st. We are deeply grateful to our talented team, incredible partners and investors, and our amazing shoppers that made this possible. While this wasn’t the way we wanted to end this journey, we are confident that our vision of bringing the store to where people live, work and play will live on through other amazing companies, products and services.’”

Comments: The crisis driver of timing makes quick changes. If a business is coincidentally positioned to take advantage of a crisis or if they can act fast, they can win. If not, as with Stockwell AI, they run out of time and fail.

“Much of what I’ve written is perhaps obvious; to me that lends credence to the idea that Clubhouse is onto something substantial. To that end, though, why now?

“One reason is hardware:

“Clubhouse is the first AirPods social network.

“The fact that Clubhouse makes it so easy to drop in and out of conversation is matched by how easy AirPods make it to drop into and out of audio-listening mode.

“An even more important reason, though, is probably COVID. Clubhouse launched last April in the midst of a worldwide lockdown, and despite its very rough state it provided a place for people to socialize when there were few other options. This was likely crucial in helping Clubhouse achieve its initial breakthrough. At the same time, just because COVID helped Clubhouse get off the ground does not mean its end will herald the end of the audio service, any more than improved iPhone cameras heralded the end of Instagram simply because its filters were no longer necessary; the question is if the crisis was sufficient to bootstrap the network.”

Comments: This reasoning was incomplete. True, the COVID crisis did create an opening for a new behavior, but people eventually became tired of it. The market window opened and then shut out of apathy. As market windows shut for social/behavioral timing drivers, there are those that represent long-term change (new sustainable addictions) and those that don’t result in enduring behavioral change. But I’m biased on this one as well, since the first iteration of an old startup of mine was a Clubhouse precursor — in a 2G world. The iPhone camera to Instagram comparison also needs to acknowledge that people stay on networks even when the initial technology advantage (the filters in that case) are no longer a differentiator.

“For Media And Gaming, Virtual Reality Is The Wolf Standing Just Outside The Door”

“[W]e’ve heard the enthusiastic cries for VR for decades. Is it for real this time?

“For the last 20 years VR has been just around the corner, but there have been three major hurdles in the way to mainstream adoption. Today, all three hurdles have been removed.

Price: “With free systems on the low-end, and a 10x reduction on the high-end, the price hurdle has finally been bested.”

Content: “The number of VR projects doubled year-over-year at this year’s E3 2015, rising to 30 new projects or titles. Every trend points to content gaining momentum. The content hurdle has also been crossed.”

Fragmentation for production and distribution: “Unity has tackled this problem head-on with their platform production tools for VR. The app stores for iOS and Android have solved the distribution problem on the low-end, and each high-end manufacturer is racing to establish themselves as a high-end, Valve-like distribution channel.”

Comments: The adoption of VR has so far been much lower than expected. The argument in the article from 2015 quoted above is one of the most important I’ve listed. We can see that simply checking off items needed to make a business work technically is not enough. With the hurdles to mainstream adoption removed (as claimed), why did VR not grow?

To compare what actually happened, here’s the Google Trends graph of interest in YouTube 360 Video, starting from the date the article was written.

Note also that the article’s author is Roelof Botha. This is the same investor who so presciently assessed YouTube’s potential in 2005.

This is a format I developed and have run with startups in incubators and accelerators, grad students, and other groups. The goal is to understand how timing may benefit a specific business or product and then how to express that. I use something that I call a Timing Map to help organize the information and understand its impact.

This entire exercise can be done in a few ways. Regardless of how much time you take for the steps, I recommend each step in the following order. I also included suggested time allotments and team member involvement. This is based on what has worked for me and the groups I’ve guided.

Form the team for the Why Now Session. That’s the founders for early-stage startups, CXOs for later-stage, and the product team for larger entities.

Form the team for the “Challenge Session.” These are the people who will pick apart your reasoning. The team could be made up of colleagues and friends for early-stage startups, colleagues across the organization and outside the organization for later-stage startups, and product leaders for larger entities. (I’ll cover the Challenge Session in a later post.)

Run the Why Now Session (advance preparation plus 1 – 2 hours of live meeting time).

Share findings with the Challenge Team. This can be either live (15 minutes) or sent in advance for individual review.

Challenge Team session. Present and take questions (1 hour total, with only 15 minutes needed for presenting and the rest of the time spent on questions).

Run the Why Now Session

1. Go through the list of drivers from the earlier posts. Which drivers are most important to your business now? Make a list of them.

If you end up with a long list, narrow down to the most important ones. Start to list the information relevant to your Why Now, including dates.

What relevant history should you know about? What earlier attempts were there at similar products?

What future expectations do you have? What will change because of the drivers you identified?

Most Relevant Drivers

Relevant History (Make a list of earlier attempts that didn’t work and why. Or earlier attempts that did work, but in a limited or different way. Include dates.)

Future expectations (Depends on driver type and expected speed of change. Include expected dates.)

“Driver 1”

“Driver 2”

“Driver 3”

2. Draw your own rough diagrams based on the drivers, using the ones below as examples. Since your situation probably includes multiple drivers, draw these however it’s most helpful to tell the story of what is changing. To keep your work readable, create a separate diagram for each driver.

For example, if your Why Now depends on a new technology becoming faster and cheaper, what’s the expected timeline for that?

For example, if your Why Now depends on a new social/behavioral norm, when did it become a noticeable niche? When might that norm become mainstream, if it hasn’t already?

3. Build the Timing Maps. Put each driver on its own timeline and show examples of the changes. You might show some distinct changes like this. Choose to put “today” at a spot that gives you enough room for the earlier examples. It’s OK if different charts have different total years of past history shown.

4. Related to the above, if you have a continuous change, rather than individual examples, you might show that change like this.

5. If you have examples of earlier companies that tried similar ideas, place them on a timeline. What happened to them? Did they fail because of bad timing?

6. If there are current companies building similar solutions, place them on another timeline. Again, choose where to put “today” so that you have enough room for the examples.

7. Now that you have done the above, mark these next points on your timelines:

The latest point at which you believe you would still be so early that your business would fail mainly because of timing. When were the drivers too weak to matter?

You can also draw a second line where you feel the market window will close based on how fast things are changing. This is where you expect other companies will dominate the industry if you don’t act. Being too late may be less of a problem than being too early.

Drivers may operate on different timelines. You’ll see below that I break them out separately and then stack them up to show the overall picture.

Also, some of these diagrams are loosely defined. When you do this exercise, it’s going to show your perspective, not a single true or false answer. You do however need to back up your perspective with data.

After this exercise, you can present all of this detail in a single slide when you pitch for investment or present your company. But the result of this exercise is that when you do speak about your business and its timing benefits, you’ll be able to have a much deeper discussion about your perspective.

Here’s an example with a large, successful company to gain more familiarity with the process.

Case Study: YouTube’s Why Now

Whenever I read about a process, I wish there were examples to help take me through them. I feel like I only really understand what to do once I see it in action. So if you’re like me in that respect, this next section is for you.

Let’s take YouTube, which was launched as a startup in 2005, to demonstrate the above technique.

Why was YouTube’s timing great? It might be hard to think back to why.

We take for granted that we can find and stream a video of just about anything today. That wasn’t always the case. What drivers impacted YouTube’s launch?

The following info is from both the Viacom Vs Google (YouTube) lawsuit that exposed Sequoia’s investment memo and other research on the companies and technologies mentioned.

1. Scanning the list of timing drivers, these look like the most important for YouTube.

Most Relevant Drivers

Relevant History (Make a list of earlier attempts that didn’t work and why. Or earlier attempts that did work, but in a limited or different way. Include dates.)

Future expectations (Depends on driver type and expected speed of change. Include expected dates.)

Technology: Moore’s Law

Falling cost of data storage needed for video files. Cost of storage for typical short videos (only 7 Megs at the time) was much less than $0.01 in 2005.

Expected to continue to decline. Data storage cost projections are available.

Technology: Edholm’s Law

Increasing data speeds for streaming large video files. By 2005 it’s already common for people to have broadband in the home. Broadband to the home grew at over 30% per year in the lead up to 2005, with approximately 30% of US households having broadband by 2005. Cost of bandwidth for typical short video files was much less than $0.01 in 2005.

Expected to continue to decline. Projected along Edholm’s Law curve.

Social/Behavioral

More people comfortable with sharing images and videos and videoing themselves.

Relevant acquisitions: Picasa (digital photo organizing service launched in 2002) was acquired by Google in 2004, Snapfish (online photo sharing and printing) was acquired by HP in 2005, and Flickr (photo sharing site launched in early 2004) was acquired by Yahoo! in 2005.

Expected to continue. People will not stop sharing online as it becomes easier to do so. People already sharing images will start to share video.

Social/Behavioral

Social networking sites like MySpace, Friendster, LinkedIn, and Facebook launched in 2003 and 2004 and are growing in popularity.

Expected to continue. These social networking sites will drive both supply and demand of online video.

Installed Base

Webcams connected to a computer became common with sales in the tens of millions of units sold by 2005.

Expected to become more popular as they become cheaper and better.

Installed Base

Digital camera (can be carried around and then connected to a computer to upload files) unit shipments were approximately 60M in 2004 and 65M in 2005, globally.

Expected to become more popular as they become cheaper and better.

Regulatory/Legal

Problems distributing copyrighted content. Avoid the issues in the beginning, with the understanding that a solution will be needed eventually.

YouTube did have to deal with pirated copyrighted content later, but since the company focused on user generated content, this area is unimportant for the Why Now analysis.

Not a top driver of timing.

2. Draw diagrams for the above list.

If any of these stopped growing, which would have the biggest impact on YouTube?

Draw projections (dashed lines) based on industry reports and the likelihood that the trend would continue.

Input your own perspective as well.

3. Now let’s look at why earlier attempts partially succeeded or failed. What has changed since then?

Earlier attempts at video streaming include:

The band Severe Tire Damage played the first Internet concert in 1993. This was broadcast live at Xerox PARC with video and audio carried over the highspeed MBONE (IP Multicast Backbone) and using a significant amount of all Internet bandwidth available. The band then opened for The Rolling Stones in another online show in 1994. Sound and video quality was poor.

Real Networks RealVideo Player (1997) could stream video and vary the number of frames per second depending on connection and computer processing power.

Blockbuster / Enron Broadband Services (2000, not launched) focused on the distribution of existing copyrighted content. Required a TV and a device.

Hong Kong Telecom iTV (1998 to 2002) required TV, a set top box, and high-speed Internet. Users experienced long delays when trying to load videos and little content to choose from.

Shareyourworld.com (1998 – 2001) enabled users to upload and share their own videos. The company was without a revenue model and had bandwidth problems, but benefitted from cameras becoming cheaper.

4. Competitors. Now add the recent companies (in 2005) delivering similar services.

PutFile launched early 2004. Provided video hosting, with ratings.

Vimeo launched in late 2004. Some problems with the technology, owned by CollegeHumor, which helped with distribution.

Google Video launched early 2005. Targeted existing content, rather than user generated content.

24 Hour Laundry (24HL) launched in 2005. Focused on video hosting and blogging.

Dailymotion launched in 2005.

Other video companies focused on adult content and were unlikely to move to the mainstream market. I’m not counting them in the list.

5. Build the Timing Maps. Make diagrams of the main drivers. For each chart I marked Too Early (dotted vertical line). In the competitor chart I marked the opportunity bracket (the space between Too Early and estimates for when the market window will close, shown by the other dotted line at the right). Today (the year 2005) is shown in bold.

YouTube also made good decisions. Helping with distribution, YouTube transcoded different video file formats to compressed Flash video, the most common format at the time. Other video companies of YouTube’s era made tactical errors, had poor management, or didn’t improve their slow video load time. Those examples are important, but aren’t included in the Why Now Session, except as additional context.

Depending on who you present to, you might not want to share all the details that came out of your Why Now Session. As a summary, put your findings in a readable single slide when you pitch for investment or present your company. The result of this exercise is that when you do speak about your business and its timing benefits, you’ll be able to have a much deeper discussion about your perspective. If desirable, you can also share the extra content in a more detailed presentation.

Now that we’ve done YouTube’s Why Now Session, what would a summary slide look like? Here’s my version.

When you compare this slide with all the detail in the above sections you can see that I chose not to include every detail. After all, when you present your Why Now slide you’re getting into a discussion, not putting every piece of supporting detail on one page. But with the more detailed work above, you will be able to discuss each of the slide’s bullet points in detail. Skip the above steps and you’ll risk a superficial understanding of your timing advantage. By going through the above process you’ll also have the content for a more detailed version that you might want to share with some audiences, such as your Challengers.

Feel free to say hello here or at @porlando on Twitter. I hold “Why Now” workshops periodically. Contact me to learn about the next one.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

In the timing or “Why Now” research I’ve been writing about I do ask you to know about existing and forecasted demand for related products. But this is different from looking at research that predicts demand for your own product.

In your supporting research, you should look at what’s changing in drivers that support your business arriving at the right time. Look at the converging factors that make this the right time for a product to exist. (Of course, you might find that there are no drivers in your case.)

But sometimes people are tempted to look at the timing question in an unhelpful way.

One tempting approach when running a Why Now Session is to look up analyst reports of future demand for your product, choose the big numbers, and use that to support your case.

Don’t do that. Here’s why.

Below is a series of analyst estimates from 2016 for the potential size the virtual reality and augmented reality market would reach in a few years. I chose 2016 since VR and AR received a lot of attention then. That was the year many people expected the technologies to break out.

“[T]he market for VR products and technologies was valued at $1.37 billion in 2015 and is expected to reach $33.9 billion by 2022. The overall market for AR was valued at $2.35 billion in 2015 and is expected to reach $117.4 billion by 2022.” [MarketResearch.com]

“The virtual and augmented reality market will reach $162 billion by 2020.” [Business Insider]

“Forrester’s report estimated the demand for virtual reality headsets in the U.S. will mean there’ll be 52 million devices in the country by 2020.” [CNBC]

“According to the report, the global virtual reality (VR) market was valued at approximately USD 2.02 billion in 2016 and is expected to reach approximately USD 26.89 billion by 2022, growing at a CAGR of around 54.01% between 2017 and 2022.” [Globe Newswire]

The above reports were from 2016. Now let’s look at reports published in 2020 about the actual current state of VR and AR.

“The global virtual reality software and hardware market size was valued at $2.6 billion in 2020, which will jump to $3.7 billion in 2021, $4.6 billion in 2022, and 5.1 billion by 2023 (SuperData, 2020). As of 2020, 26 million VR headsets are owned by consumers globally (CNBC, 2020). The combined augmented reality and virtual reality markets were worth $12 billion in 2020 with a massive annual growth rate of 54%, resulting in a projected valuation of $72.8 billion by 2024 (IDC, 2020).” [Finances Online]

“The global virtual reality market is projected to grow from $6.30 billion in 2021 to $84.09 billion in 2028 at a CAGR of 44.8% in the forecast period, 2021-2028.” [Fortune Business Insights]

5.5 million VR and AR devices were shipped globally in 2020. [IDC]

What wildly different outcomes in just four years! The expectations from 2016 were much higher than what reality served up in 2022.

My point isn’t to pick on VR and AR market analysts. There have been many industries that seemed promising and ready for fast growth that later fell short of expectations. Instead, my point is that if you’re using other people’s forecasts to justify your own timing, you’re skipping the process and just looking for big numbers to legitimize what you’ve decided to do anyway.

You are also missing the point of thinking about timing and running a Why Now Session. You need to approach the Why Now Session from the perspective of learning about drivers that support your business, not by simply choosing research that agrees with you.

Plus, if you just repeat analyst quotes, when you meet someone who doubts the numbers, the best response you can give is “that’s what they say.”

But why were the analyst reports wrong?

It’s hard to know without seeing their process, but I suspect something other than methodology as the prime cause.

What gets reported and repeated are the big numbers, the big potential opportunities, the stories for how the world will be different in the near future. Teams seeking investment and even investors seeking justification for their investments will be tempted to stress the optimistic outlooks. So will analysts. It’s more noteworthy to publish research claiming a big change is on the way, rather than research saying that the world will remain the same.

Avoid copying analyst research outright and focus on understanding timing drivers and their impact on your business.

If you’re presenting your own Why Now, relying on analyst reports without understanding the underlying drivers opens you up to being challenged by someone who doesn’t believe the reports. Instead, if you present your reasoning behind the way drivers will affect outcomes and the timing for that, you’ll have a discussion.

I’ve done a YouTube timing analysis from the perspective of 2005. In that case I did use analyst reports on the number of projections, including on digital cameras and webcam sales, how broadband penetration was going to grow, and on the cost of file storage. I also showed what people had already done, such as the number of cameras purchased and social media and online image sharing that was already taking place.

But there were a couple differences in the YouTube research I used and the VR / AR examples I showed above.

For some of the research I showed, the world had already reached the point where enough supporting drivers were in place. File storage was already cheap, even if it was declining in cost predictably. Broadband penetration to the home was already becoming common and people were not about to go back to dial-up. Digital cameras and webcams were already becoming common and the idea that people would go back to videocassettes was unlikely.

The supporting drivers were already in place and demand for video was already there.

That list is different from the VR / AR projections for units shipped, which made projections on what people would start to do in the future.

If you’re evaluating someone’s Why Now and you question them using a set of analyst reports you trust, make sure you understand the drivers of the expected changes.

If you’re evaluating someone’s Why Now and you instead see a reliance on analyst reports, talk through their logic.

If someone pushes back on your Why Now with an analyst report that they trust, ask how the analyst came to their conclusions. Is the disagreement on how fast the change will happen or on its magnitude? Is there an appreciation for the way multiple drivers may converge?

Simply reporting that a changing industry will be a certain size by a specific date doesn’t give you much useful information.

Feel free to say hello here or at @porlando on Twitter. I hold “Why Now” workshops periodically. Contact me to learn about the next one.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

In the previous post on Why Now: Timing and Product Success I introduced 12 timing drivers. That list of drivers was Technological, Social/Behavioral, Regulatory/Legal, Installed Base, Economic, Networks, Distribution, Capital Access, Organizational, Available Talent, Demographic, and Crisis.

These are the drivers that help you determine if what you are building is going to hit the market at the right time.

To get a better feel for them, I like to visualize the way those drivers behave. Here they are with some simple diagrams that explain more about how they work.

And this is part art, part science. I’m writing this series because as important as the Why Now question is, I haven’t seen many people dive into the question deeply. I’m trying to do that over a series of posts and workshops.

Select from this list and add to it depending on your situation.

Technology drivers change what you can build. What was too slow, too expensive, or impossible becomes fast, cheap, and possible. Here are a couple examples.

Economic drivers reflect changes in the economy you operate in. They are usually not smooth changes – at least not for long. Shocks are common.

Regulatory and legal drivers describe the way businesses are prohibited or required because of governmental decisions. Some types of businesses and products are strongly prohibited, only to be allowed later on. Sometimes those prohibitions or requirements operated cleanly – like an on/off switch. And sometimes there’s a lot of flexibility. In those cases, regulatory/legal drivers are more like a dimmer switch.

In some cases, there is predictability to these changes. An example of clean predictability is when something is patented, allowing the patent holder to commercialize it while preventing others. But patents are for a limited number of years. Some industries only grow when key patents expire.

Less predictable changes include new legislation that is influenced by public interest groups or lobbyists, changing public opinion, and elections that affect who votes on rules.

As for the dimmer switch, some rules are just loosely enforced.

Social and behavioral drivers can offer surprises.

There are enduring human needs that seem like they’ll never go away, as long as there are people. A short list would include love of music and entertainment and the need for housing and food.

There are also habits that emerge or are promoted. Over the centuries, people started drinking coffee and tea – old products that have been commercialized in increasingly more ways. People also started to drink alcohol in many forms, sometimes commonly in the evening and at other times and places in history, from breakfast until dinner. What determines those changes?

Installed Base drivers rely on the existence of another product that the new business will ride on top of.

Devices in use may perform a vital function that enables something new.

Different from Installed Base, Network drivers create opportunities through their connections.

Network drivers are affected by the number of nodes, connections between them, and how communication flows.

Organizational drivers are about the way people organize themselves and resources. Innovations in these drivers affect what can be built and how.

New types of Distribution, both physical and digital, make new businesses possible.

What Available Talent is there to support the building of specific products? What will these people need as they take new roles?

Demographic Drivers describe the way populations change over time. Some changes are predictable in advance (you need 25 years to grow a new group of 25 year olds). And some change over time.

Capital Access changes over time with the economy, interest rates, evidence of success stories, and other trends.

And whatever the situation, a Crisis can change things quickly. Crises can change the speed and direction of processes and result in unexpected outcomes.

These are examples. Your experience may not be described above. But you can use the categories to explore which drivers impact your business and what specifics you see in each.

Feel free to say hello here or at @porlando on Twitter. I hold “Why Now” workshops periodically. Contact me to learn about the next one.

Deciding what product to build depends on many things. The problem you’re trying to solve, your capabilities, what you’re passionate about, people involved, how much time you have, your budget, and even temporary considerations like what’s currently hot and how easy it is to raise money.

You have similar questions if you’re evaluating startups as potential investments. Or if you’re a startup founder or an early team member. Or even if you’re part of a team in a larger organization developing new products in-house.

Many things influence your likelihood of success, but there is one factor we recognize, while often not really diving into how it works. That’s the importance of timing, or the “why now” question.

This question has become common in the startup world, but is relevant in many situations.

Forms of the Question

Depending on your focus, the Why Now question itself can take different forms.

“Why is this the right time to build this business?” In other words, what bigger forces support this type of business being a success?