If you’re finding this post now, I actually wrote a book about all this… It’s called Why Now: How Good Timing Makes Great Products. You’ll get a fuller perspective there.

In the last few posts I introduced the idea of why timing is important, the 12 timing drivers I track, and why you can’t just use analyst reports to figure things out. I also showed how I run “Why Now” sessions.

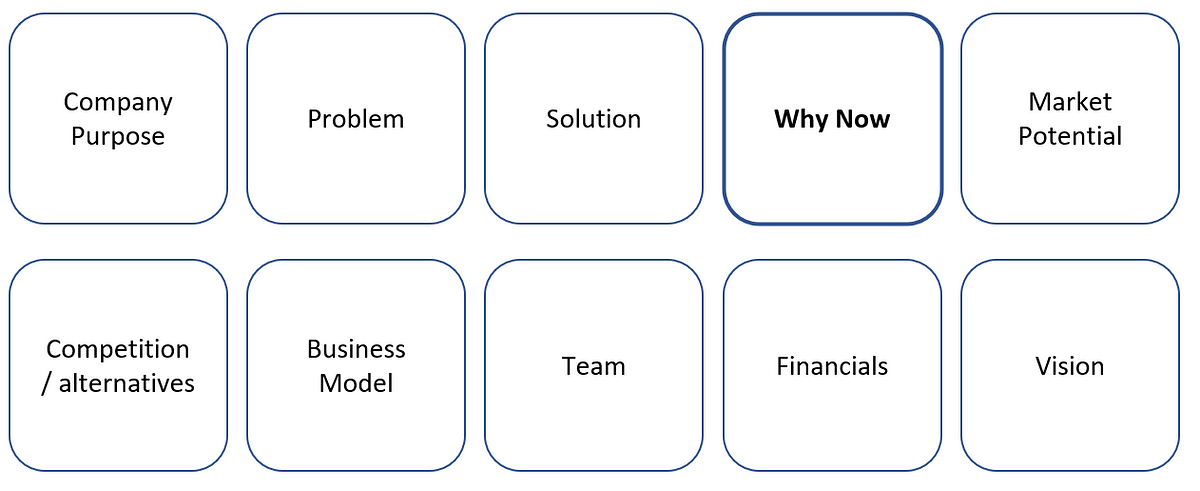

Now let’s look at the way people have presented timing advantages. Below is a collection of:

- Why Now slides from pitch decks (26 examples)

- Sequoia startup founders on the Why Now question (6 examples)

- Interviews with founders, investors and more about timing (12 examples)

- Weak Why Nows and companies that failed because of or in spite of timing (6 examples)

Why Now slides from pitch decks

I believe that your perspective on timing is one of the most important pieces of insight you can bring to the discussion with an investor or when discussing resources and direction internally.

As I demonstrated in the earlier posts above, you need to do your own research to have a perspective. And while you’ll summarize your timing advantage in a single slide, you should start with that more detailed research. Otherwise, you won’t be able to answer investor and management questions (and your slide will be superficial).

Powerful startup Why Now slides explain why this business is in the market at the right time (and why a few years ago would have been too early). What has changed? What timing drivers opened up a market window that the startup is now exploiting? The slide is typically placed after the problem and solution slides.

This is a collection of slides from actual startups, all publicly available online. I show just the relevant slide the company used in their deck and also add a quick assessment.

I take the slides at face value but I’m not claiming that these examples are perfect. In some cases I critique them or question the assessments. This is an exercise to understand how startups expressed their own timing advantage. In some cases, I show how the Why Now assessment ended up being incorrect.

The images link to the full decks.

AdPushup

Comments: This slide relies on analyst forecasts and (at the time) hotness of the adtech market. If you can move fast, you might be able to take advantage of a hot market. But if things outside of your control change, what do you do then? Think a step earlier to what drives the expected growth. The A/B Testing comment is more focused on open space in a market where experience from another market can be applied.

Bliss AI

Comments: Interesting from today’s perspective that Bliss AI was focused on remote work back in 2015 and listed a projection for the year 2020. Rather than use projections of how big remote work would become, think about what drives the change.

Crossbeam

Comments: This is a list of strong drivers that demonstrate why the time is right. The slide also shows how the drivers collide to produce an even stronger effect. Go into more detail on expected growth in due diligence.

Databricks

Comments: Connecting the need to build AI/ML solutions with these four categories makes this a strong slide. The commoditization category is especially interesting.

Dropbox

Comments: Good list. In discussion, the founders can explain just how cheap storage and bandwidth have become (this slide is from 2008) and how that makes a new business model possible.

Dutch

Comments: Good assessment of what changed because of the pandemic, how that impacts pets, and what will further change when people go back to the office rather than work at home.

Enduring Planet

Comments: This startup makes make rapid financing available to climate entrepreneurs. Is the focus on the interest in climate change enough of a timing driver? They also provide a simple diligence and investment process which isn’t common. Could they claim that tech also adds to their “why now”? This is one of the simplest Why Now slides I’ve seen. It could go a lot further.

Fivetran

Comments: Good list, but what is changing with these tech drivers? Why wouldn’t this business have worked a few years ago?

Glambook

Comments: Rather than quote a projection, what drives the increase in self-employment for their targets? It’s unclear what will change by 2027. Weak slide.

Harvest Money

Comments: Do these numbers represent a tipping point? Were the debt numbers of a few years earlier too low for this business to be built? Otherwise, if it didn’t matter in the last recession, why is it different now?

Kahani

Comments: Might be a good opportunity, but I’m not sure about the why now claims. Why did mobile ecommerce survive so long without changing? Seems more about straightforward performance of this solution. Why are ecommerce sites going to change now?

Lunchbox

Comments: The driver is entirely about existing and projected market size. What else is relevant here? Why will this market growth continue? Will growth continue post-pandemic?

Lunch Club

Comments: It’s a list, but if these changes have been ongoing, why do they matter now?

MetaCert – In-App Security

Comments: Interesting point that thanks to the growth in DIY app builders there will be demand for security, or at least fixing security problems. (But if the point is that creation is exploding, I don’t see it in the image.)

MetaCert – Team Collaboration Security

Comments: This would be stronger if it explained how this risk is growing. Haven’t companies dealt with this security risk for years at this point? What changed? Was a tipping point reached? A regulatory change?

Momentum

Comments: This slide is from 2022 and so it leaves a lot unsaid. Remote work and reliance on remote tools are now norms. Did this business require the Covid push to remote work?

National Virtual Observatory

Comments: Strong. These changes enable this business (slide is from 1999). Without these timing drivers the outcomes would be dramatically more expensive and less powerful.

On Deck

Comments: Strong list that supported their fundraising efforts in 2021. But did traditional higher education really decline as ed-tech grew? And while that Peloton example stings from the viewpoint of 2022, it did the job then they wrote this list. A strong Why Now also doesn’t mean that the team won’t mismanage their opportunity later on.

Party Round (now called Capital)

Comments: A simple slide that tells the story. Verbally fill in the details about how fast these alternatives are growing.

Shift

Comments: If the used car market has doubled in the last decade, will growth now slow down? Is the online research done more often today than previously?

Snyk

Comments: Good combination of timing drivers. The “New Kingmakers” one is interesting because it combines existing tech talent with a new responsibility.

Standard Treasury

Comments: Simple list. The big question is whether the company can move in line with the regulatory changes. What else about the tech maturity and growing market would be relevant?

Sunshine

Comments: The biggest timing driver here is the increase in smartphones with built-in sensors.

Supliful

Comments: These may be facts, but what changed? Was there a tipping point reached in number of creators? Did creators become more relatable than brands just recently? Otherwise, it seems that this business could have been started years earlier.

Vori

Comments: Many startups benefitted (or suffered) because of the sudden onset of Covid, lockdowns, and supply chain problems. If a business happened to be well-positioned to benefit from such changes or was able to adjust quickly, this crisis provided a strong timing advantage. The question is then what happens when things go back to the way they were?

Yapily

Comments: This is a full look at drivers behind this company’s existence. The main one is probably the regulatory change.

Here’s a breakdown of each of the above slides, by the 12 timing driver categories I track.

Sequoia Portfolio Company Interviews

The following are interviews focused on the startup “why now” question that Sequoia investors did with their portfolio companies. Snippets of the conversation are below along with video links. These are all from 2018. The update comments are limited to additional funding rounds or acquisitions as a sign of whether the companies continued on the right track.

Wonolo (on-demand staffing for businesses)

“The problem of unpredictable staffing has been around forever. It’s not new. What’s new is that with the increasing adoption of mobile technology and the rise of the on-demand economy, we’re seeing a paradigm shift in that people are trusting an app to find workers and jobs.”

Update: Raised $140M in 2021, a few years after the above.

Front (customer communication platform)

“Before, companies were just using email to get organic and now they have Twitter and Facebook and Snapchat and text messages and so on. So they need to centralize everything in one place because those are just different ways to do the same thing: communicate. And that’s what Front does.”

Update: Raises a Series D at 1 $1.7B Valuation in 2022.

rideOS (mobility-as-a-service technology).

“As you look back at transportation over the last few decades, there’s been three megatrends that are completely changing the way that people and goods move throughout the planet. The first one was electrification. We had great companies like Tesla bring that technology to market. The second one was ridesharing and concept of sharing cars. And companies like Uber, Lyft, and Didi brought that technology to market. And a third one has been autonomous technologies. How to effectively utilize technology to drive on the road. And there’s been significant investments into the third bucket over the last few years. But most of that investment has been focused on how to get one vehicle to market. As we look towards the path that this technology is taking and we look at a world that is filled with millions of self-driving vehicles and other forms of transit, like buses, and MRT stations, and taxis, and also other forms of transport, there needs to be a type of air traffic control system for ground transport. And that’s where rideOS comes in. We’re looking at the problem of taking fleets to market and building marketplaces and mapping services to help bring that system to the world in a safe and efficient manner.”

Update: Acquired by Gopuff for $125M in 2021.

Cobalt Robotics (after-hours security robot service)

“We’re at a unique time in technology where we have all these amazing component technologies that are very cost-effective today. To basically be able to allow an autonomous mobile agent to move very reliably and very safely through human spaces. That’s something that just wasn’t possible 10 years ago that is now very much achievable.”

Update: Raised another $35M in 2019.

NEXT Trucking (digital marketplace for trucking)

“90% of our industry is comprised of small trucking companies, either owner operated or small fleet. Lack of transparency and yield mandates actually make our existing trucker shortage problem more severe now. And NEXT Trucking actually increases our carry efficiency by connecting them with their preferred loads and then we also help our industry supply and demand.”

Update: Later raised at a $500M valuation in 2019.

Snowflake (cloud computing)

“Because it really wasn’t possible to build Snowflake before now. The cloud made Snowflake possible and with Snowflake companies can work with vast amounts of data. And all of the people within an organization and even across organizations can work together.”

Update: Later raised another $480M and then IPO’d in 2020.

Interviews and Articles

This is a collection of interviews and articles where the timing question comes up.

Torc Robotics

“Why now for the automotive push? Torc CEO Michael Fleming told me that the time is finally right, both in terms of the state of available technology, but also in terms of the appetite for autonomous products from consumer automakers — which weren’t always as eager to develop and invest in self-driving.

“What we’ve found is that were some other markets that were early adopters to this technology, and there wasn’t a great deal of interest in the automotive industry coming out of the DARPA Challenge,” explained Fleming. “Google is really the early adopter of this technology, with some key folks from the Carnegie Mellon and Stanford teams from 10 years ago, and they’ve done some great marketing, and they’ve been on the forefront of this technology in the automotive space.”

Comments: The timing question here refers to Torc’s push into automotive, having already built other autonomous applications.

“Regulations can define the best places to build and invest”

“In April, the White House announced a target for the U.S. to reduce greenhouse gas pollution by at least 50% by 2030 and achieve net-zero emissions by 2050. The guidance includes a vision for more investment in building a transmission grid, electric vehicles and charging infrastructure, and carbon capture tools, and enabling farmers to foster sustainability in soil.

“In aggregate, the support of the public sector streamlines private-market solutions through access to alternative (often equity-free) capital and press recognition, which is crucial for a market that typically requires longer time to monetization and profitability.

“Ultimately, the regulatory fabric is an important market maker or breaker. That is true for nascent companies searching for answers to the “why now?” of market timing and also for established, public companies that are answering strategic questions of how much more they can grow.”

Comments: Regulations and top-down support are an influence on timing advantages.

“4 strategies for deep tech founders who are fundraising”

Answer the question of “why now?”

“Being right but too early or too late is the same as being wrong in the investing world. Early-stage venture capital investors operate on seven to 10 year time horizons with their investments because that is the timeline they have for each fund to return capital to themselves and their limited partners (those who invest in venture capital funds). If your company can only be a huge success 15 or 20 or 50 years from now, venture capitalists would still not invest because this return would not be realized on their target timeline.

“As a result, it is crucial to discuss not only why your idea is great but also answer the “why now.” Deep tech companies have more of a why now than companies in most other sectors. There are technological inflection points and regulatory tailwinds that make the timing perfect for deep tech companies.

“Dedicate a slide to explaining how macro and industry level tailwinds make now the ideal time to start your company. Articulate why your innovation could not have been achieved before today and why tomorrow would be too late.”

Comments: Framing timing in the seven to 10 year investment horizon is interesting. It’s also a reason that startups needing more time need to seek different investors.

“General Catalyst’s Niko Bonatsos on why timing and empathy are key to founder success”

“Q: If you were to pick one and only one single biggest factor that determines a startup’s success, what would it be? Why? Some say it is product-market fit (Marc Andreesen), others hold that it’s timing (Bill Gross) and yet more believe it is the team. Asked another way, what do you think is essentially different about successful startups?

“If I had to pick one, I’d pick timing. But again, it could be explained as foresight or genius of the founder to launch the startup at a great moment in time.

“The most successful companies have a confluence of factors aligning to work in their favor. Take Facebook, for example. Mark Zuckerberg founded it at a time when everyone was getting online and broadband was becoming pervasive.

“In contrast, some really talented and hardworking founders just happen to work on the wrong things and don’t attain the same level of success. Some even tried Zuck’s idea but were too early. It often isn’t their fault. The timing just wasn’t right.”

Comments: Another investor perspective on timing.

“Mural raises $23M Series A after history of capital-efficient growth”

“Gaddy also answered the why now, and why so much question, saying that Mural is riding a ‘secular trend in terms of how people are going to produce creative work.’

“Mural is a tool that can be seen as a remote-work-friendly service. It’s also workplace collaboration software, putting it smack-dab in the middle of two current trends in Startuplandia.”

Comments: This is from a January 2020 article, just before Covid sent work to default remote. Mural benefitted both from the long-term trend and the sudden crisis change.

“VCs have to train themselves to ‘ask the stupid questions,’ says Hoxton Ventures’ Hussein Kanji”

“I think it’s actually perfectly fine in the venture industry to not be the smart person and to kind of train yourself to be stupid and ask the stupid questions,” said Kanji. “I think a lot of people are probably too shy to do that. And a lot of people [are] probably too risk averse to then write the check when they don’t really understand exactly what it is that they’re investing into. But a lot of this stuff is a light bulb moment.”

“One of those light bulb moments was Hoxton Ventures’ investment in Deliveroo, the takeout food delivery service that competes with Uber Eats and helped turn almost every restaurant into a food delivery service. However, Kanji reminded us that the European unicorn wasn’t the first company to try takeout delivery, but new technology, in the form of cheap smartphones coupled with GPS and routing algorithms, meant the timing was now right.

“‘People did try delivery,’ he said, ‘they tried it back in the 90s. Everyone forgets about that. There’s a company in New York City called Kozmo that would go off and like get you a pint of ice cream on demand. You know, it never worked because they used pagers. Like, do you remember pagers?… The breakthrough for delivery, and for that whole industry, was you had smartphones, you could give smartphones to the drivers, you could track what the driver was doing, which is good because then you could route logistics, you know, with a smartphone… light bulb moment.’”

Comments: A common timing example involving GPS-enabled smartphones.

“YC-Backed SpinPunch Aims To Build Faster, Prettier HTML5 Games”

“Mars Frontier is certainly an impressive game (albeit one that I sort of suck at), but I had to ask: why HTML5? Why now? Tien thinks the shift toward building more compelling browser-based gaming experiences is a matter of course, but doesn’t see too many players in the space really trying to push HTML5’s limits….

“It’s just a matter of time before the entire games industry moves to the browser, since the distibution [sic] advantage is so powerful,” Tien noted. Though the potential for tremendous reach is there, the shift isn’t going to happen overnight, but SpinPunch seems intent on riding the bleeding edge until it does.”

Comments: A new technology driver coupled with existing demand.

“Fin names former Twilio exec Evan Cummack as CEO, raises $20M”

“‘Service teams were forced to go remote overnight, and companies had little to no visibility into what people were doing working from home,” she added. “In this remote environment, we thought that Fin’s product was incredibly well-suited to address the challenges of managing a growing remote support team, and that over time, their unique data set of how people use various apps and tools to complete tasks can help business leaders improve the future of work for their team members. We believe that contact center agents going remote was inevitable even before COVID, but COVID was a huge accelerant and created a compelling ‘why now’ moment for Fin’s solution.’”

Comments: Crisis as an accelerant on what was going to happen anyway. Crisis sometimes operates differently and makes a change in outcomes, rather than just speeding them up.

“Q3 2020 is primed to be an intense shopping season for VCs”

“You have to include a “why now” slide and it should mention COVID-19.

“We already know that investors respond well to a Why Now slide. Our research shows that 54% of successful pitch decks included a Why Now slide, where only 38% of failed decks included it. That slide now has to work twice as hard. We’re hearing from investors that they expect to see information in your pitch deck about how your business has been affected by COVID-19 and how you plan to manage that impact moving forward. Even if the pandemic has had no material effect on your business, the investor will still have the question. Get out in front of it with a well-formed response near the beginning of your deck.”

Comments: Seems obvious now, but Covid became the big change of 2020. Everything was filtered through that crisis.

“Nest Team Descends On Nike Town To Recruit Fuel Band Engineers”

“Nest, the connected device company that was acquired by Google for $3.2 billion, apparently needs all the hardware engineers it can get. As the core hardware group within Google, Nest will be spearheading the development of new hardware products.

“That could mean phones, or tablets, or… wearables?

“So it’s probably not a surprise that members of the Nest team paid a visit to Beaverton, Ore. yesterday to have an informal meet-and-greet with folks who might have been part of the Nike Fuel Band team….

“Which is why now is a great time for other hardware companies to give them some options, by trying to recruit them.”

Comments: Good to move quickly when a crisis (the Nike lay-offs) combine with a lack of talent in a specific desired domain.

“Whistle While You Scroll, Or, How Facebook Could Conquer Music Videos”

“Suddenly, it seems like everyone wants to host music videos. Apple features them in Apple Music, both as suggestions of what to listen to and as posts from artists in the Connect tab. Spotify recently announced it would start showing video clips inside its app. New apps like Vessel are trying to court indie musicians and their videos with better revenue sharing. The labels still run their own hosting platform Vevo that often fueled by YouTube’s player. And YouTube is trying to monetize music videos more aggressively with its YouTube Music Key ad-free paid subscriptions.

“Why now? Mobile has come of age for video. Phones unlock the little five-minute wait times in our lives, and prime them for content consumption. Faster network connections, bigger screens, and more powerful processors all mean the videos load and look better. And advancements in mobile advertising make them monetizable.”

Comments: This article was written in 2015. Since then, Facebook did go much more heavily into video, but also faced competition from other video-first companies.

“How Can We Help? Announcing Signia’s 2nd Fund”

“The “Why Now?” helps us understand the market conditions that now make it possible for the potential investment to have global impact. We’re looking for cash-efficient disruption of large existing markets or the creation of new ones. Broadly speaking, we invest in technology companies that are taking advantage of mobility and data. Mobility to us means not just the rise of the smartphone as the dominant computing platform, but also new technologies such as Virtual Reality and Augmented Reality (VR/AR). Data doesn’t just mean Hadoop, it also means companies that are helping others take advantage of the huge surge in all different types of data being collected or delivered (from commerce to commuting to mobile video delivery). Many of the sectors we invest in are just starting to tap into their potential for huge impact, including transportation, fintech, commerce, VR/AR, big data, mobile SaaS, and AI. Check out the ideas section of our website for other areas we’re looking at.”

Comments: From 2016, this article focuses on the way an investor looks at timing.

Weak Why Nows

Having a timing advantage is not a guarantee of success. There are lots of ways to miss an opportunity. We also have to be sure that we don’t just cherry-pick the best examples.

But there are also lots of ways to invent a timing advantage when there are none. Is there anything in common when we see this happen?

“Source: Facebook Is Testing ‘Facebook At Work’, Separately Hosted Version To Roll Out In A Few Months”

“Enterprise social tools have existed for years. When I asked why now, the source told me it was simply because Facebook now had the infrastructure in place to support such a system”

Comments: The infrastructure rationale is weak. If Facebook didn’t have the infrastructure, would they built it for this product?

From “The Top 12 Reasons Startups Fail”

Starsky Robotics

“Timing, more than anything else, is what I think is to blame for our unfortunate fate. Our approach, I still believe, was the right one but the space was too overwhelmed with the unmet promise of AI to focus on a practical solution. As those breakthroughs failed to appear, the downpour of investor interest became a drizzle.”

Comments: In my other work on the timing topic, this is where we see the expectation of a process that seems to be improving on an exponential curve instead flattens into S-Curve. The needed improvements are still years away. Early companies shut down or burn cash seeking the improvements they need to bring their product to market.

Vreal

“VR platform Vreal intended to build a virtual reality space for video game streamers to hang out with their viewers and raised almost $12M in its 2018 Series A. However, the available hardware and bandwidth capabilities didn’t evolve as fast as the company had expected, and though it delivered on its promise, Vreal struggled to attract any significant usage:

“Unfortunately, the VR market never developed as quickly as we all had hoped, and we were definitely ahead of our time. As a result, Vreal is shutting down operations and our wonderful team members are moving on to other opportunities.”

Comments: I read this as mostly the result of a lack of demand. What could have given the team and investors this insight ahead of time?

Stockwell AI

“For some companies on our list, an unforeseen factor like the Covid-19 pandemic contributed to product untimeliness. AI-powered vending machine startup Stockwell AI shut down in July 2020 as consumers stayed at home and avoided surface contact. The company’s CEO Paul McDonald wrote in an email to TechCrunch,

“’Regretfully, the current landscape has created a situation in which we can no longer continue our operations and will be winding down the company on July 1st. We are deeply grateful to our talented team, incredible partners and investors, and our amazing shoppers that made this possible. While this wasn’t the way we wanted to end this journey, we are confident that our vision of bringing the store to where people live, work and play will live on through other amazing companies, products and services.’”

Comments: The crisis driver of timing makes quick changes. If a business is coincidentally positioned to take advantage of a crisis or if they can act fast, they can win. If not, as with Stockwell AI, they run out of time and fail.

Read here (all of the above section)

“Clubhouse’s Inevitability”

“Much of what I’ve written is perhaps obvious; to me that lends credence to the idea that Clubhouse is onto something substantial. To that end, though, why now?

“One reason is hardware:

“Clubhouse is the first AirPods social network.

“The fact that Clubhouse makes it so easy to drop in and out of conversation is matched by how easy AirPods make it to drop into and out of audio-listening mode.

“An even more important reason, though, is probably COVID. Clubhouse launched last April in the midst of a worldwide lockdown, and despite its very rough state it provided a place for people to socialize when there were few other options. This was likely crucial in helping Clubhouse achieve its initial breakthrough. At the same time, just because COVID helped Clubhouse get off the ground does not mean its end will herald the end of the audio service, any more than improved iPhone cameras heralded the end of Instagram simply because its filters were no longer necessary; the question is if the crisis was sufficient to bootstrap the network.”

Comments: This reasoning was incomplete. True, the COVID crisis did create an opening for a new behavior, but people eventually became tired of it. The market window opened and then shut out of apathy. As market windows shut for social/behavioral timing drivers, there are those that represent long-term change (new sustainable addictions) and those that don’t result in enduring behavioral change. But I’m biased on this one as well, since the first iteration of an old startup of mine was a Clubhouse precursor — in a 2G world. The iPhone camera to Instagram comparison also needs to acknowledge that people stay on networks even when the initial technology advantage (the filters in that case) are no longer a differentiator.

“For Media And Gaming, Virtual Reality Is The Wolf Standing Just Outside The Door”

“[W]e’ve heard the enthusiastic cries for VR for decades. Is it for real this time?

“For the last 20 years VR has been just around the corner, but there have been three major hurdles in the way to mainstream adoption. Today, all three hurdles have been removed.

Price: “With free systems on the low-end, and a 10x reduction on the high-end, the price hurdle has finally been bested.”

Content: “The number of VR projects doubled year-over-year at this year’s E3 2015, rising to 30 new projects or titles. Every trend points to content gaining momentum. The content hurdle has also been crossed.”

Fragmentation for production and distribution: “Unity has tackled this problem head-on with their platform production tools for VR. The app stores for iOS and Android have solved the distribution problem on the low-end, and each high-end manufacturer is racing to establish themselves as a high-end, Valve-like distribution channel.”

Comments: The adoption of VR has so far been much lower than expected. The argument in the article from 2015 quoted above is one of the most important I’ve listed. We can see that simply checking off items needed to make a business work technically is not enough. With the hurdles to mainstream adoption removed (as claimed), why did VR not grow?

To compare what actually happened, here’s the Google Trends graph of interest in YouTube 360 Video, starting from the date the article was written.

Note also that the article’s author is Roelof Botha. This is the same investor who so presciently assessed YouTube’s potential in 2005.

Here’s the list of other Why Now posts. If you like these, check out the Why Now book.

- “Why Now: Timing and Product Success”

- “Avoid the Analysis of Others (Why Now)”

- “Running a ‘Why Now’ Session”

- “50 Timing Examples (the Why Now question)”

- “Measuring Your Market? Consider Timing.”

- “What People Miss About Timing”

- “What Others Say About Timing”

- “The ‘Cold Market’ as the Next Hot Market”